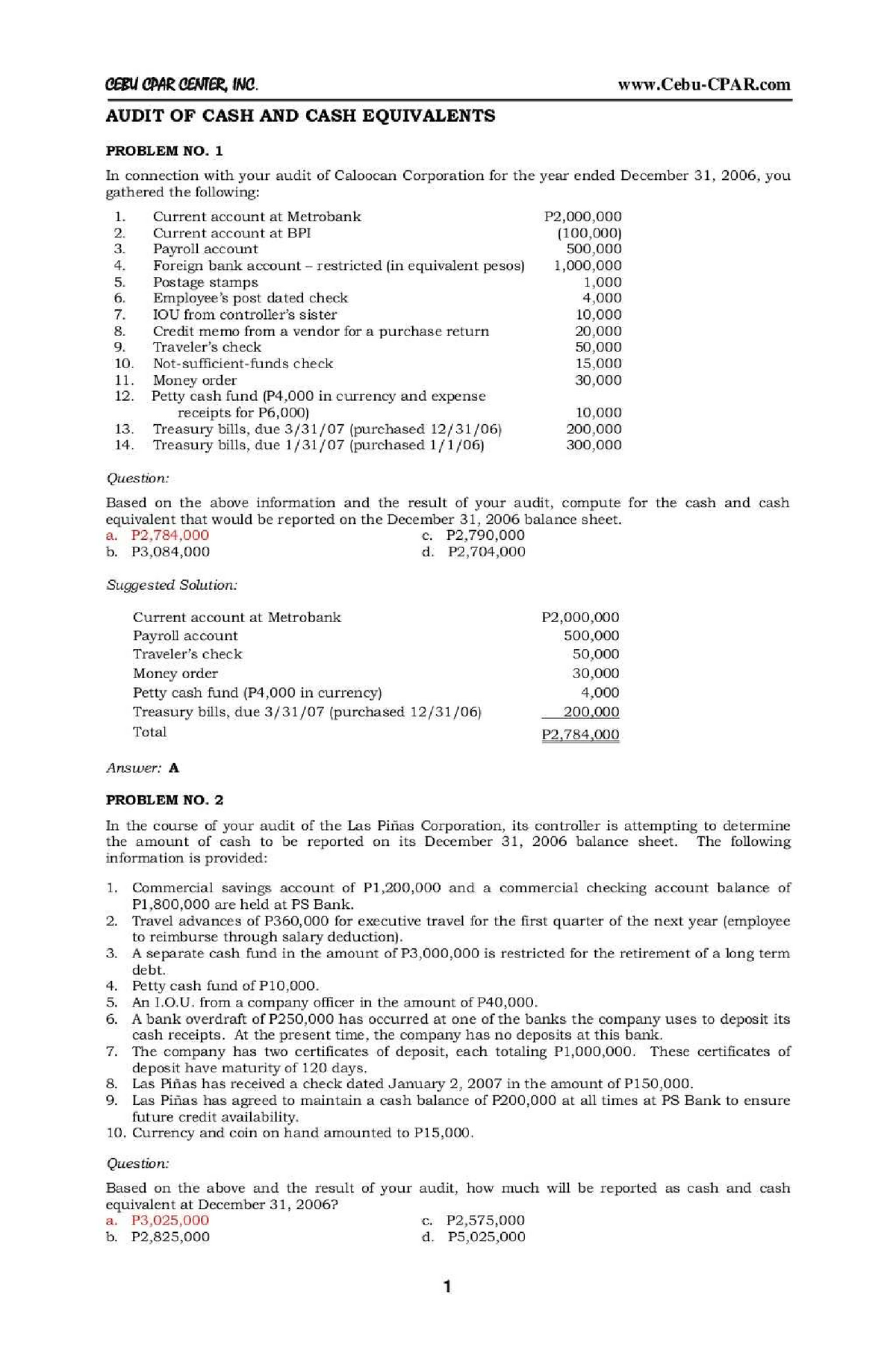

Outside of the most recent credit score matter, the brand new good facts hardly amount so you can consumers. It might started once the one thing of a shock, although way more you are aware regarding metrics in it, the greater your odds of efficiently increasing your credit score.

A credit rating constantly refers to another person’s FICO Rating, therefore always involves several anywhere between 300 in order to 850 one ways your own creditworthiness. Users dont always apply at one of several around three big revealing organizations to own lots tasked. As an alternative, this happens naturally because you remove funds, take on credit card also provides, and pay back this type of an excellent otherwise constant bills.

Beyond financial obligation payment records, teams you to definitely influence your credit score and see debt-to-money percentages, exactly how many productive accounts, and other affairs. According to such, credit agencies project less credit history amount if you have terrible creditworthiness and you can increased credit score amount for those who pay-off bills promptly, keeps suitable loans-to-earnings percentages, and now have sufficient sense handling loans precisely to show creditworthiness.

What exactly is good credit?

You will need to remember that lenders features various other mortgage being qualified requirements. Regional borrowing unions generally speaking offer extremely competitive cost consequently they are known be effective specifically tough to let neighborhood players, even people with less-than-best borrowing from the bank. That said, the fresh new both discreet differences between being qualified to own a loans Shoal Creek car loan, mortgage, or lower-focus bank card can be difficult. This new standard solution to what exactly is good credit sleeps towards the lender’s requirements. Of numerous financing associations score credit rating conditions such as the following.

- Poor: 3 hundred so you’re able to 579

- Fair: 580 in order to 669

- Good: 670 so you’re able to 739

- Decent: 740 to help you 799

- Excellent: 800 so you can 850

Lenders essentially thought people who have a credit rating regarding 670 otherwise large once the lower-chance consumers. People with straight down scores under 670 may be viewed as subprime individuals and be susceptible to large interest levels and less versatile payment terms and conditions. The greater the FICO score, the much more likely you are so you can qualify for low-notice mortgage products. That is why understanding the factual statements about how to build borrowing from the bank and you can raise your FICO rating are very important for your requirements along with your family members’ financial health and wellness.

If you’re looking to possess a for the-breadth need out of credit rating selections, comment our blogs, “What exactly is a good credit score? Credit history Variety Said”.

What is a beneficial FICO Get

Brand new Fair Isaac Corp delivered the fresh FICO rating during the 1989 because the a method to measure individual creditworthiness. Brand new terms FICO get and you can credit score turned into relatively similar even with almost every other teams issuing different designs. More Fico scores follow the 300 to 850 variety, with a few globe-specific ratings carrying out as little as 250 and you will peaking on up out-of 900.

However for standard purposes, a buyers who would like to can build borrowing from the bank and you may enhance their FICO rating is generally better made by understanding how the number are determined. These represent the baseline products you to influence their FICO rating.

- Fees Record: The 3 big credit agencies typically legs 35 percent from your own FICO get into the repayment history. That it ranks just like the biggest measurable part of the equation.

- Obligations Relative to Borrowing Limits: How much cash your borrow secured on present credit constraints and additionally performs a good large character. Credit rating dresses assign a 30 % worth in order to borrowing incorporate whenever determining a FICO get.

- Chronilogical age of Profile: The average period of your membership additionally the length of time you centered borrowing from the bank possess a beneficial fifteen % influence on the FICO get.

- Borrowing from the bank Software: When individuals sign up for money otherwise playing cards, an excellent tough inquiry otherwise tough eliminate is done on your own history. These types of brings on your own credit history make up 10% away from new computation and will negatively effect a FICO rating to possess upwards so you can half a year.